How Much Does a Cosigner Help on Auto Loans?

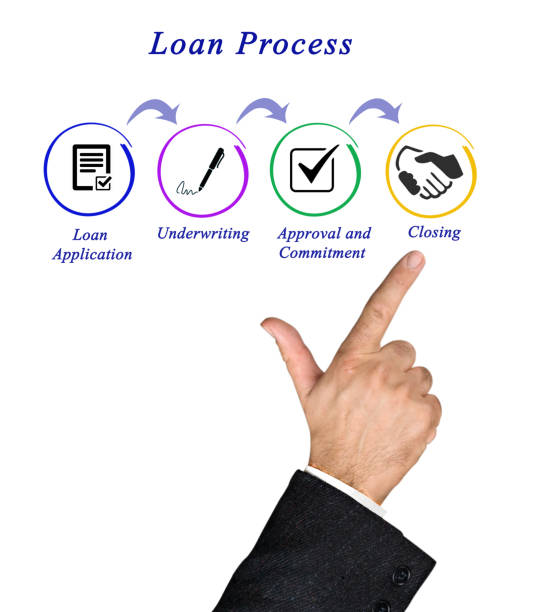

How much does a cosigner help on auto loans? This article explains what a co-signer is as well as how a co-signer can help make an auto loan approval process easier.

Finding an auto loan with an inexpensive monthly installments may be difficult if your earnings is restricted or your credit score requires to be improved. Nevertheless, using a co-signer on your loan could really be helpful.

When you use a co-signer, your loan conditions are probably significantly better because the earnings and credit history of that person are taken into account.

Most times, your chance of approval or denial can depend on whether you have a co-signer or not.

ALSO READ:

Will Geico insure a car not in my name?

How to use EIDL loan for self-employed?

What Is a Co-signer?

A co-signer, together with the original borrower, assumes complete accountability for loan repayment.

Most times, a co-signer is usually a close relative. In the event that the borrower defaults, the co-signer may be required to cover all unpaid payments as well as the entire loan balance.

If the borrower fails pay back on time, the credit of the co-signer may likely suffer. Making use of a co-signer on your loan provides the lender more confidence that the loan will be paid back.

How Much Does a Cosigner Help on Auto Loans?

Applying for a car loan with a co-signer can greatly strengthen your application and, eventually, enhance the loan conditions you are given.

This is very important for individuals with poor credit scores who might just be starting to establish their credit history and have little to no payback history for lenders to analyze.

When you use a co-signer, the application additionally takes into account that person’s earnings and credit profile.

In other words, a prospective lender will consider the capacity of your co-signer to pay back the loan in full by themselves.

You have greater chances of being granted favorable loan conditions if your co-signer has a decent credit score of 670 or above and a bigger earnings than you do.

This is due to the fact that using a co-signer provides the lender with additional security that the loan will be paid back even if you are unable to make payments.

Advantages of Having a Cosigner on an Auto Loan

Therefore, what is a cosigner’s role in a loan? The function of a cosigner is to affix their name to a car loan application along with the loan itself in order for the main borrower to receive approval.

For borrowers with minimal to no credit record, a cosigner could be necessary to boost the likelihood of being approved, although this depends on the lender.

The exciting thing is that cosigning has advantages for you as well if you have been requested by someone to be his or her co-signer.

Your credit score will rise so far the main borrower makes monthly loan repayments promptly.

However, you might experience a few of the disadvantages of cosigning if things do not always go well as planned.

ALSO READ:

What increases your total loan balance FAFSA?

How to get prescribed antidepressants without insurance

Disadvantages of Having a Co-signer on an Auto Loan

Although a cosigner is intended to aid a borrower with bad credit in getting loan approval easily, the dangers associated with the setup make some people uneasy with it. Cosigning has 3 key disadvantages:

Cosigner is compelled to Pay If the Main Borrower Fails to Make Payment

In the event that the main borrower is late on payments or fails to repay the loan, the cosigner will be held accountable by the lender for payments and will be compelled to make up for any damages.

Any issues will also have an impact on the cosigner’s credit score since they are risking their own credit for the main borrower.

Applying For Additional Lines of Credit Might Be Impacted

When a cosigner consents to cosign a loan, the loan appears as a liability on their credit reports.

This implies that the lender will count the cosigned loan as extra debt if the cosigner intends to acquire a fresh line of credit.

Although the cosigner may not be paying off the loan currently, the lender will take the loan payment into account when calculating their debt to income ratio.

This can make it harder for them to get other loans while the auto loan is still outstanding.

It Is Difficult to Remove a Cosigner

Refinancing is the only possible means to get rid of a cosigner from a loan.

Thus, following the cosigner’s signature on the document, there is no turning back. If the credit of the main borrower has not increased during the loan’s term (often essential to be eligible for the car’s refinancing), it’s possible that the cosigner will be saddled with it until the car is paid off.

NOTE: The easiest approach for a cosigner to prevent any financial issues is to stay in touch with the main borrower.

Ensure they make their payments on time each month, and ensure you and they come up with an arrangement if they require assistance before any payments are skipped and the lender comes after you.

Co-signers and Minimum Income Requirements

In order for loans to be approved, lenders often have minimum income requirements. The lender will majorly take into account your earnings as the main applicant when figuring out if you satisfy such standards.

The earnings of your co-signer won’t be taken into account in this application section. The earnings of your cosigner is not summed up with your own to assist you reach the minimum income requirement.

Nevertheless, if you were to fail for whatever cause, your co-signer would need to demonstrate that they have sufficient money to cover the monthly vehicle payments by themselves.

The main thing a prospective vehicle purchaser needs to know is that a co-signer is probably not the answer if they require extra money to be eligible for a loan.

What is the Difference between Co-signing and Co-borrowing?

Having a co-signer on your loan varies greatly from having a co-borrower, which is occasionally also known as a co-applicant.

You must comprehend the differences between these two methods of buying a car. If you have a co-signer, that car does not belong to that person in any way.

They only consent to intervene and take responsibility in the event that you fail to repay your auto loan.

Meanwhile, a co-borrower is a person who is a joint owner of the vehicle. The co-borrower is equally liable for the payments same way you are from the time the loan is started.

Furthermore, when obtaining a loan alongside a co-borrower, every property utilized as collateral for the loan, like a house or vehicle, might be owned by both co-borrowers.

Keyword: How much does a cosigner help on auto loans

When You Should Not Have a Co-Signer on an Auto Loan

You have to thoroughly examine using a co-signer to obtain approval on an auto loan before submitting application.

It might not always be the best course of action given your demands and financial circumstances. Here are a few instances of when you should not have a co-signer on an auto loan:

You Can’t Afford the Vehicle

It’s preferable to avoid buying a vehicle entirely if the price of the vehicle is not what you can afford regardless of whether it has a reduced interest rate.

You might consider delaying on purchasing the vehicle until you have enough funds saved for a greater down payment in order for the loan amount to be in accordance with your monthly spending plan and earnings.

If you want a car urgently, another alternative is to search for a secondhand vehicle at a cheaper rate.

You may additionally wish to consider whether you can increase your credit score, which ought to enable you to negotiate a lower interest rate and a relatively reasonable loan installments.

There May Be Tension in Your Relationship

If any issues in your relationship develop, having a co-signer on an auto loan might be a precarious situation.

If you default on the loan payments and your co-signer is compelled to step in and pay back the loan on your behalf, it could put a lot of tension on the relationship.

Keyword: How much does a cosigner help on auto loans

Conclusion

It can be simpler to get approved for an auto loan if you have a co-signer to assist you with the application.

Most times, you’ll get a loan with better loan conditions, which may lower your monthly payment and increase your ability to purchase the vehicle.

This may be useful especially if you’re just starting to establish a credit profile or if your credit score is not too excellent.

Nevertheless, prior to utilizing a co-signer to move through with applying for a loan, think about your alternatives.

For example, you might save up more money for a bigger down payment in order for the buying of the vehicle to be cheaper for your budget or raise your credit score to acquire a better favorable interest rate.