How to Use EIDL Loan for Self-Employed?

How to use EIDL loan for self-employed? This article explains everything about EIDL loans including how to use it as a self-employed person.

Several American businesses are finding it difficult to secure the funding they require to remain viable as the worldwide pandemic continues in high gear.

Furthermore, because it is unknown how long the pandemic and the downturn it caused would persist, numerous small business owners could be worried concerning the fate of their businesses.

The Small Business Administration (SBA) has intervened to assist with a loan program that can provide assistance to companies experiencing difficulty during the COVID-19 outbreak.

In the event that you are self-employed and were successful in obtaining a loan through the Payroll Protection Program (PPP) or an Economic Injury Disaster Loan (EIDL) to lessen the financial effects of COVID-19, it’s crucial to comprehend how they can affect your taxes as well as any prospective debt forgiveness.

ALSO READ:

What can EIDL loan be used for?

Can you apply for EIDL loan twice?

What Is the EIDL Loan Program?

The Economic Injury Disaster Loan (EIDL) program is a loan program backed by the SBA. Small companies, micro agricultural enterprises, and the majority of private organizations in a disaster region that have sustained significant financial harm are eligible.

A company may be qualified for an EIDL loan to ensure its survival if a disaster prevents it from covering its regular overhead cost and it is unable to obtain financing from any other means.

Despite the fact that majority of business owners knew about it due of COVID-19, the EIDL program is not something that recently came out.

Before the pandemic, the loan program provided loans with reduced interest to companies and homeowners who were impacted by natural disasters including wildfires, landslides, and storms.

But lately, the emphasis has been on helping companies affected by the coronavirus. There had been over 1.7 million EIDL loans granted by June 2020, and that figure is still growing.

Irrespective the loan’s widespread use, many people who are self-employed could still have a number of concerns regarding what they can or cannot do with the EIDL loan.

Knowing the terms and conditions of an EIDL loan is essential if you’re considering asking for one in order for you can make sure you’re utilizing the money legally.

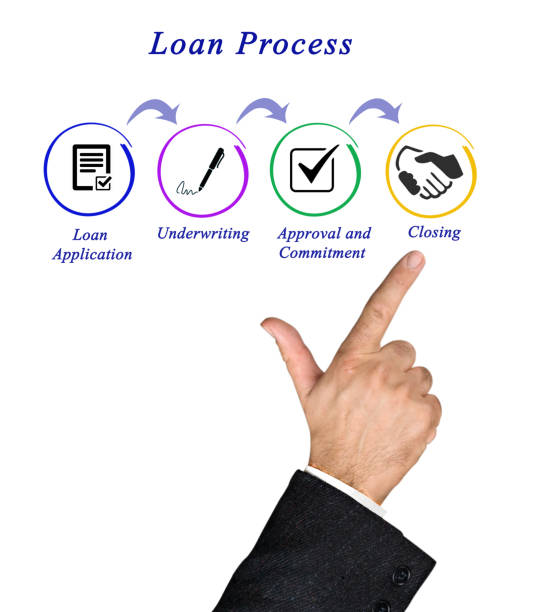

How Does an EIDL Loan Appear?

When you’re considering applying, it’s useful to be know the explicit boundaries that the government sets for EIDL loans.

The most you could borrow with an EIDL loan is $2 million. This comprises loans under the COVID-19 EIDL as of September 8, 2021.

An EIDL loan may have an interest rate as high as 3.75%. The interest will start to accumulate even though your first payment will not be due for a year (or two years for a COVID-19 EIDL loan). You can begin your loan’s repayments lot quicker.

The longest length of an EIDL loan is 30 years, during which you must repay the money in addition to interest and charges.

Depending on your circumstances, different amounts and other conditions could be applicable to you.

For loans over $25,000, collateral is necessary; and property is the recommended type of collateral.

What Are the Uses of EIDL Loans?

EIDL loan usage restrictions appear straightforward on the outside. However, it’s crucial to comprehend them completely.

Funds from loans can be utilized by companies for working capital or regular operational costs such as:

- Perks for workers’ health

- Wages

- Rent

- Utilities

- Changing out inventory

- Recurring debt payments

- Maintenance

Remember that applicants must certify that they will utilize the money only to cover EIDL-qualified costs to mitigate any financial damage induced by the disaster.

To make it easier for you to show how the money were utilized, the SBA advises putting your EIDL money in a bank account that is different from your other money.

The uses of COVID-19 EIDL loan have been widened as of September 8, 2021, to cover payback of commercial loan as well as payment of federal business loan.

ALSO READ:

Can credit card companies garnish your wages?

Are small business loans installment or revolving?

What Are the Limitations on EIDL Loans?

Generally, there are certain things you are not permitted to utilize EIDL loans for, such as:

- Refinancing fresh loan

- Purchasing major commodities, new buildings, or cars

- Settling past due debts

- Rewards and distributions

- Payments to owners except for performance of services

- Payback of principal loans or shareholder loans (with some limitations)

- Payment of a direct federal debt apart for IRS obligations

Consult the SBA for clarification if you are unsure about a particular cost.

How to Use EIDL Loan for Self-Employed?

Some small business owners who are self-employed could be asking if they qualify for EIDL loans and how they may utilize it.

Identifying their income might be one issue they have. Several business owners choose to make a deduction against total earnings as opposed to receiving a wage.

According to the SBA, lenders can utilize tax returns and bank statements to confirm an applicant’s earnings in either situation.

In addition, whether it is for a worker or a self-employed person, the expenses below can be funded by an EIDL loan:

- Insurance costs

- State and local taxes

- Paid salaries, royalties, profits, or net revenues (up to a maximum of $100,000 per worker)

- Employee perks (holiday, family, and sick leave expenses)

- Retirement perks

Self-Employed People and EIDL Loans

If you are a self-employed person with staff and you are looking for extra funding because of COVID-19, but you did not secure a PPP loan, you might wish to think about submitting an EIDL application to the federal Small Business Administration (SBA).

The $484 billion extra COVID-19 assistance plan, which was authorized in April, included an extra $60 billion to cover Economic Injury Disaster Loans (EIDL).

Furthermore, the SBA is providing loan advances to eligible applicants who choose this alternative because of the economic problems brought on by COVID-19.

They must have your bank’s routing number and account number in order to deposit the loan advance.

Wages, recurring debts, accounts payable, and any costs that you couldn’t cover immediately as a result of the effect COVID-19 can all be covered with an EIDL.

Apart from the forgiven amount, your EIDL will be repaid at an interest rate of 3.75% within a maximum of 30 years.

The conditions contain a default one-year postponement on payback, during which time interest will continue to accumulate.

Should I Apply for EIDL Loan?

It’s important to decide if the SBA EIDL loan is appropriate for you since you are aware of what it can be utilized for.

There are some small business loans have conditions as enticing as those of an EIDL loan. The current interest rate on the loans is 3.75%, and the payback period can last a total of 30 years.

After the note’s issuance date, you have a year without payments due on your EIDL loan; and a repayment plan will be provided to you after the loan is approved.

You are free to submit an application for the EIDL program online. You will need to provide some details about your company on the application, such as:

- Kind of business

- Employer Identification Number or Social Security number

- Total earnings for the year prior to the pandemic

- Price of commodities sold for a year prior to the pandemic

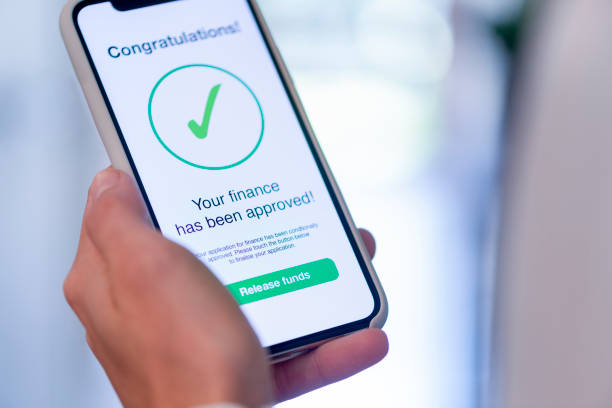

Reviewing applications requires at least of 21 days. The money will be paid into your bank account if you are accepted.

Please be aware that the SBA won’t take applications for COVID-19 EIDLs that total over $500,000 until October 8, 2021.

What Are Other Options apart from the EIDL Loan?

If you are not interested in applying or you are not granted an EIDL loan or if the program ends, you can still want funds to keep things running while business is sluggish.

You may obtain emergency business loans, however, be aware that you can end up paying a substantially larger interest rate for the ease.

Small business owners may also want to think about the following additional kinds of funding:

- Lines of credit

- Traditional bank loans

- Business credit cards

- Merchant cash advances

- Equipment financing

- Invoice factoring and financing

Although some of these may need good credit score, others might focus more on your income than your credit.

EIDL Can Support You during Difficult Moments

You are ultimately responsible for deciding whether or not to apply for an EIDL loan. However, the EIDL can be the best option for several enterprises to obtain funding with loan agreements they would not ordinarily be eligible for.

Although, it’s true that loan is still a debt, regardless of the duration of time it will take to repay it or how much interest it has.

There may be a strong draw on your credit report when you apply for the EIDL loan, and there’s a chance that your score would lose some points.

If you are trying to improve your credit, you should be informed about this. Nevertheless, If you promptly pay the loan’s monthly installments, It can improve your credit as time goes on.

The assistance you require to get to brighter days may be found in obtaining an EIDL loan if your company has suffered as a result of the pandemic.

However if you are seeking for small business funding, you have a variety of alternative choices to consider.

Conclusion

We have come to the conclusion of this amazing article on “how to use EIDL loan for self-employed.”

If you are a self-employed individual with employees and you are seeking for additional financing due to COVID-19, you might want to consider applying for an EIDL loan.

EIDL loan is designed to provide assistance to business that were negatively affected due to the outbreak of the COVID-19 pandemic.

Despite that EIDL loans could be the best kind of financing you need for your business right now, there are some restrictions on things you can use it for.

Not all expenses should be covered with EIDL loan. EIDL loans can be used for some expenses such as Insurance costs, state and local taxes, retirement perks and many others.

As a self-employed individual, ensure you do not use EIDL loan for something it is not meant for.